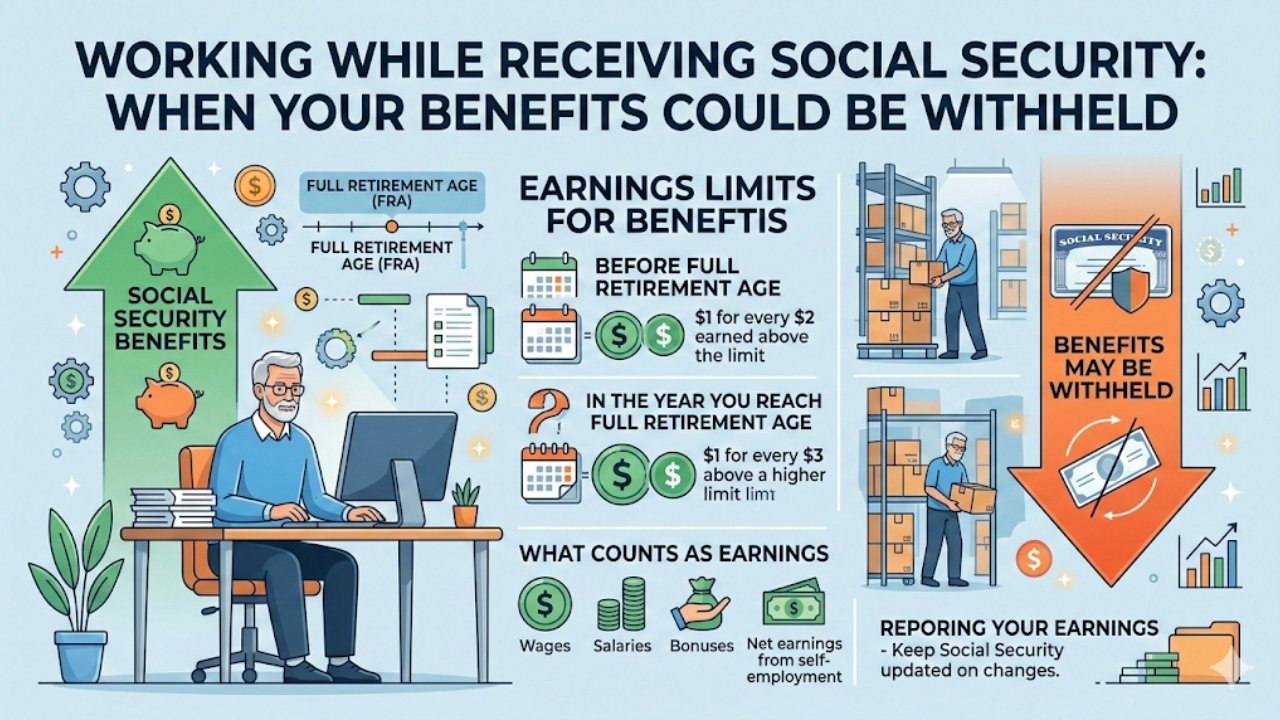

Many Americans dream of supplementing their retirement income with part-time work while collecting Social Security benefits. However, the rules around earning extra money can trip up even savvy retirees. The Social Security Administration (SSA) imposes earnings limits to encourage full retirement before claiming benefits. If you claim before your full retirement age (FRA)—typically 66 to 67 depending on your birth year—and earn above a set threshold, part of your benefits gets temporarily withheld. This isn’t a permanent loss; once you hit FRA, withheld amounts are recalculated and credited back, boosting your future checks.

The key is distinguishing between those under FRA and those at or above it. Under FRA, the SSA scrutinizes your wages closely. Above FRA, you can earn unlimited income without reductions. This system balances work incentives with the program’s sustainability, affecting millions who semi-retire in their 60s.

How Earnings Tests Work in Practice

The SSA calculates your earnings test annually, based on wages from jobs, self-employment, or commissions—but not pensions, investments, or rentals. They use your net earnings from self-employment after deductions. Only the first $1,950 of monthly earnings over the limit triggers a reduction for those in their year of reaching FRA.

Imagine a 64-year-old claiming benefits early and working as a consultant. Exceed the limit, and $1 gets withheld for every $2 over the cap throughout the year. Reach FRA mid-year? The formula shifts to $1 withheld per $3 earned above a higher monthly threshold until your birthday month. These adjustments prevent overpayments while rewarding delayed claiming.

2026 Earnings Limits at a Glance

To make this crystal clear, here’s a quick data table summarizing the 2026 limits (adjusted annually for inflation by the SSA):

| Age Group | Annual Limit | Monthly Equivalent | Withholding Rate |

|---|---|---|---|

| Under FRA all year | $23,400 | $1,950 | $1 for every $2 over |

| Year of reaching FRA (before birthday month) | $62,160 | $5,180 | $1 for every $3 over |

| At or above FRA | Unlimited | Unlimited | None |

Exceptions That Let You Keep More Benefits

Not all income counts toward the limit. Disability benefits under SSDI follow different rules, often allowing substantial work trials like Ticket to Work without reductions. Students under 22 can earn up to $2,400 annually (2026 estimate) before cuts. Self-employed folks deduct business expenses first, softening the blow.

Certain jobs, like ministers or foreign agricultural workers, have special exemptions. If you’re a surviving spouse or widow(er) benefits recipient under FRA, the same limits apply unless caring for a child. Planning ahead—perhaps timing work around your FRA month—can maximize take-home pay without surprises.

Real-Life Impacts and Strategies

Consider Maria, a 62-year-old teacher who retired early but tutors part-time. Earning $25,000 last year exceeded the limit by $1,600, so $800 in benefits got withheld. She didn’t lose it forever; at FRA, her monthly benefit rose by about $40 to recoup it. Stories like hers highlight the temporary nature of withholdings—1.5 million people faced this in 2025, per SSA data.

Smart strategies include monitoring earnings via SSA’s online portal, bunching income into FRA years, or opting for Roth withdrawals (which don’t count). Spousal benefits might offer a workaround if your partner’s record is stronger. Consulting a financial advisor ensures your work plan aligns with long-term goals.

Long-Term Planning for Maximum Benefits

Withholding feels punitive short-term but incentivizes FRA claiming, where benefits max out. Early claimants forgo up to 30% permanently by starting at 62, compounded by earnings tests. Delay to 70, and you gain delayed retirement credits—8% annually.

Work enhances your record too; higher recent earnings replace lower ones in the benefit formula. In 2026’s economy, with remote gigs booming, blending work and benefits is viable. Track inflation-adjusted limits yearly, as they rose 5% from 2025.

Navigating Changes and Resources

SSA rules evolve—2026 saw slight hikes amid wage growth. File taxes accurately; the IRS shares W-2 data with SSA for audits. Appeal errors within 60 days if withholdings seem off.

Free resources abound: SSA’s Retirement Estimator tool, mySocialSecurity account, or local offices. Nonprofits like AARP offer webinars. Stay informed to turn potential pitfalls into opportunities.

FAQs

1. Does self-employment count toward the limit?

Yes, but only net earnings after business expenses.

2. Are withheld benefits lost forever?

No, they’re recalculated and added back at FRA.

3. Can I avoid the test by delaying benefits?

Yes, waiting until FRA or 70 eliminates limits entirely.