Planning your finances for 2026 starts with understanding the fresh IRS adjustments to contribution limits and tax brackets. These changes help stretch your savings further amid rising costs, offering smarter ways to build retirement nests, fund education, and cover health needs. Families and workers alike can tweak strategies now for real gains later.

Retirement Savings Boosts

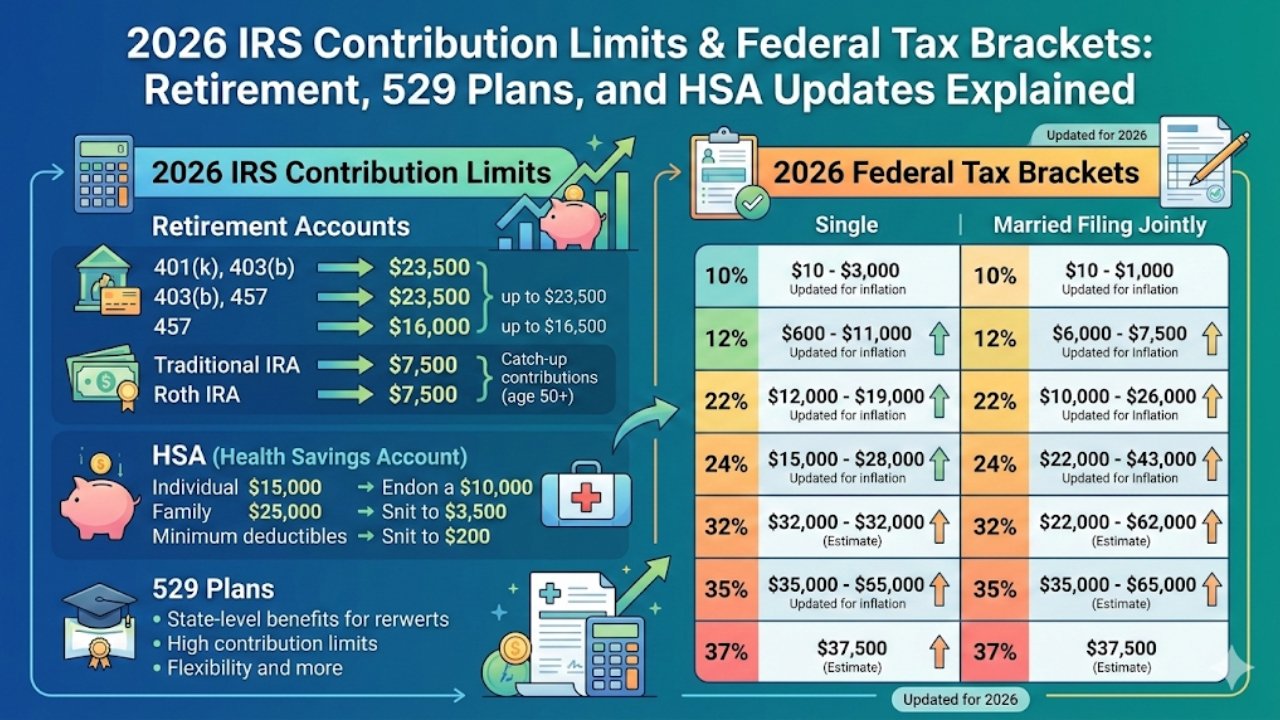

Workers eyeing retirement will notice elective deferrals to 401(k), 403(b), and similar plans climbing to $23,500, up from prior years to match inflation. Those 50 and older snag an extra $7,500 catch-up, letting seasoned savers pile in more tax-deferred dollars. Traditional IRA and Roth IRA caps hold steady at $7,000, with $1,000 catch-up for 50-plus, but phase-outs shift higher for higher earners, easing access.

Key 529 Plan Tweaks

Education savings through 529 plans stay flexible, with no strict annual cap from IRS, though states often mirror retirement limits around $7,000 per beneficiary for tax perks. New in 2026, rollover allowances to Roth IRAs expand up to $35,000 lifetime per child after age 15 in the account, taxed as income but penalty-free. This bridges college funds to personal retirement, a game-changer for over-savers.

HSA Limits Rise

Health Savings Accounts shine brighter with self-only coverage at $4,400 and family at $8,750, edging up to keep pace with medical inflation. Folks 55-plus add $1,000 catch-up, no Medicare snag. High-deductible plans qualify if deductibles hit $1,700 self/$3,400 family, out-of-pocket max $8,500/$17,000, making HSAs triple threats for tax-free growth, withdrawals, and investments.

Federal Tax Bracket Shifts

The 2026 federal income tax brackets adjust for inflation, widening bands to soften bracket creep. Singles see 10% up to $11,925, 12% to $48,475, 22% to $103,350, and top 37% over $626,350. Married filing jointly starts 10% to $23,850, stretching to 37% above $751,600. Standard deductions rise to $15,000 single/$30,000 joint, plus $1,600 extra for 65-plus.

| Category | 2025 Limit | 2026 Limit | Change |

|---|---|---|---|

| 401(k) Deferral | $23,000 | $23,500 | +$500 |

| IRA Contribution | $7,000 | $7,000 | Steady |

| HSA Self/Family | $4,300/$8,550 | $4,400/$8,750 | +$100/+200 |

| 529 Rollover Max | $15,000 | $35,000 lifetime | Expanded |

| Std Deduction Single/Joint | $14,600/$29,200 | $15,000/$30,000 | +$400/+800 |

Strategic Planning Tips

Max these limits early for compound magic—contribute biweekly via payroll to hit caps effortlessly. Roth options suit younger earners betting on lower future taxes, while traditional shines for current deductions. Bundle HSA with low-cost index funds for health costs in retirement, and tap 529 for K-12 too, up to $10,000 yearly tax-free.

Impact on Families

Families win big with doubled family HSA and joint brackets favoring spouses. Education savers redirect unused 529s without penalties, easing grandparent gifts. High earners watch phase-outs: workplace IRA deductions fade at $81,000-$91,000 single, Roth eligibility drops at $150,000-$165,000 joint, so prioritize pre-tax now.

State and Long-Term Views

While federal sets the floor, states like California may nix 529 perks or tweak HSAs—check locally in Chandigarh’s global context or U.S. filings. Long-term, these hikes signal steady inflation, urging auto-escalation in plans. Review W-4s annually; President Trump’s 2025 policies keep rates stable, but watch Congress for tweaks.

Action Steps Ahead

Lock in raises matching these limits, discuss spousal strategies, and model scenarios with free IRS withholding estimators. Early birds harvest full benefits, dodging last-minute rushes come April 2027. Solid planning turns numbers into nest eggs.

FAQs

What if I max 401(k) and IRA?

Yes, both count separately for bigger savings.

Can I contribute to HSA on Medicare?

No, enrollment blocks new contributions.

Do brackets affect my refund?

Higher brackets mean owing more if withholdings lag.