Many retirees in 2026 find they need or want to keep working after claiming Social Security benefits. This extra income can boost financial security, but it comes with specific earnings limits that affect your monthly checks. Understanding these rules helps you plan ahead and avoid unexpected reductions.

Understanding Earnings Test Basics

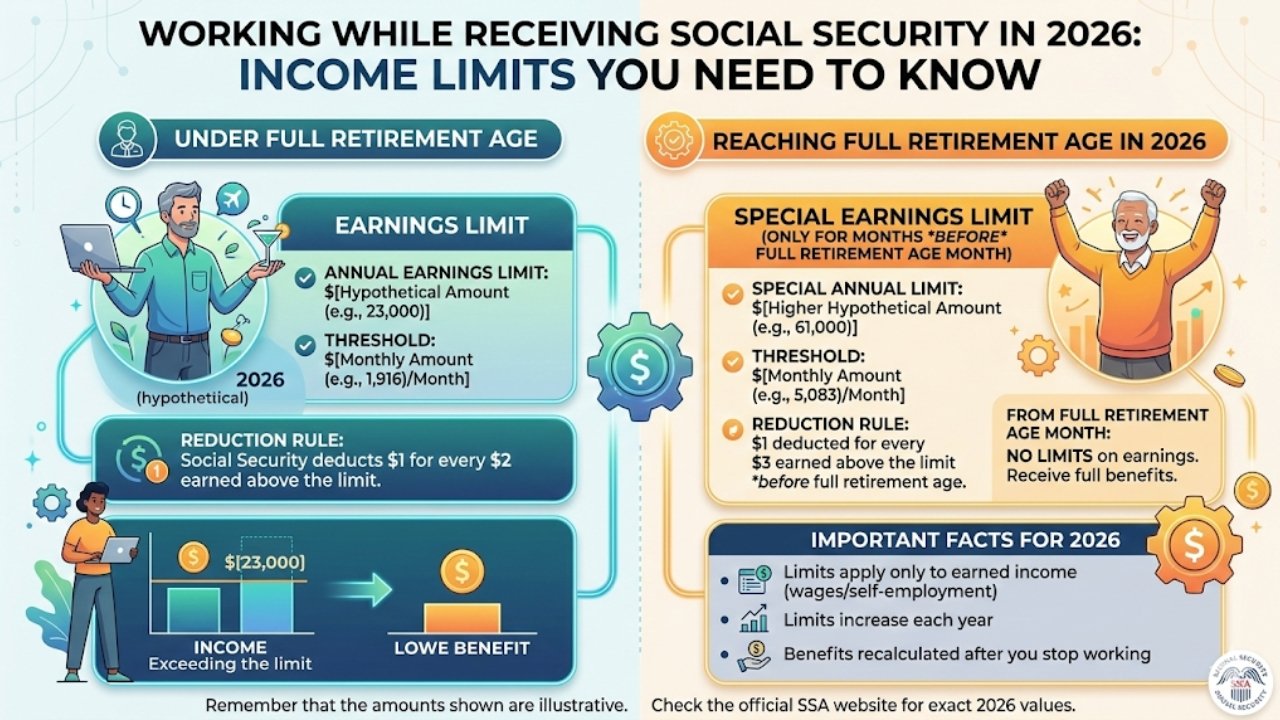

The Social Security Administration applies an earnings test to those who claim benefits before reaching full retirement age (FRA). FRA depends on your birth year—for those born 1960 or later, it’s 67. If you’re under FRA all year, earnings above a set limit trigger a temporary withholding of benefits. These withheld amounts aren’t lost forever; they’re recalculated into higher payments later.

Income from wages or self-employment counts, but pensions, investments, or other non-work sources do not. The test only applies to the year you receive benefits while earning over the limit. Once you hit FRA, the restriction lifts completely, letting you work freely without reductions.

2026 Income Limits Breakdown

For 2026, precise thresholds guide how much you can earn. Workers under FRA all year face a $24,480 annual limit—exceeding this means $1 in benefits withheld for every $2 over. Those reaching FRA during the year get a higher $65,160 cap, applied only to pre-FRA months, with $1 withheld per $3 excess.

Self-employed individuals calculate earnings as net profit minus business expenses and half of self-employment taxes. These rules ensure fairness while encouraging gradual retirement. Planning your work hours or gig economy side hustles around these numbers keeps more money in your pocket.

| Category | 2026 Annual Limit | Reduction Rate | Applies To |

|---|---|---|---|

| Under FRA All Year | $24,480 | $1 per $2 over | Wages/Self-Employment |

| Year Reaching FRA (Pre-FRA Months Only) | $65,160 | $1 per $3 over | Wages/Self-Employment |

| At or Above FRA | No Limit | None | All Income Types |

Strategies to Maximize Benefits

Timing your benefit claim around work plans makes a big difference. Delaying until FRA or beyond avoids the test entirely, and withheld benefits from early claiming get credited back with interest-like adjustments. Part-time work or seasonal jobs often stay under limits effortlessly.

Consult a financial advisor for personalized math—tools like the SSA’s online calculators show projections. Spouses or survivors have separate rules, so family dynamics matter. Reducing hours in high-earning months before FRA can preserve checks while still padding savings.

Tax Implications of Working

Extra income might make up to 85% of your Social Security taxable if combined income exceeds $25,000 (single) or $32,000 (joint). Working raises this risk, but deductions like the new 2026 senior credit—up to $6,000 ($12,000 married)—help offset it for moderate earners under $75,000/$150,000 MAGI.

Track quarterly estimates to avoid IRS penalties. High earners watch IRMAA surcharges on Medicare premiums too. Balancing work with Roth conversions or charitable giving minimizes the bite, keeping your net gain strong.

Real-Life Examples for 2026

Picture Jane, 65 with FRA at 67, earning $30,000 yearly from consulting. Over the $24,480 limit by $5,520, she loses $2,760 in benefits ($1 per $2). But credits restore this later, boosting her monthly amount permanently. Mike, turning 67 mid-year, earns $70,000 but only faces the test January-June, dodging major cuts.

Gig workers like Uber drivers tally monthly to stay compliant. These scenarios show flexibility—many thrive by adjusting schedules. Retirees often report higher satisfaction blending benefits with purposeful part-time roles.

Planning for Long-Term Success

Review your earnings record yearly via mySocialSecurity account to ensure accuracy, as it shapes future benefits. The 2026 wage base hits $184,500, capping taxes and credits for high earners. Contribute to IRAs alongside work to compound retirement funds.

Community programs and job boards for seniors offer limit-friendly opportunities. Stay informed on COLA—the 2.8% bump raises max benefits to about $5,251 monthly at FRA. Proactive steps today secure tomorrow’s stability.

Common Pitfalls to Avoid

Don’t overlook self-employment taxes or assume investment income counts—only labor does. Claiming early then stopping work triggers repayments if overpaid. Report changes promptly to SSA to prevent audits or delays.

Myths persist, like benefits stopping forever—reductions are temporary. Underreporting earnings risks fines. Double-check with SSA’s 800 number or local office for peace of mind.

FAQs

Q: Do pensions count toward the earnings limit?

A: No, only wages and self-employment income do.

Q: What if I exceed the limit one year?

A: Withheld benefits get recalculated into higher future payments.

Q: Is there a limit after FRA?

A: None—you can earn unlimited amounts.